Description

INTRODUCTION – Rolling Stock Market in India 2019-2025

The Indian Railways contributes to ~3% of the country’s gross domestic product (GDP) and has social obligations pegged at $5.3 Billion annually. Indian Railways revenue has grown at 5% CAGR in the past 5 years but profitability has reduced drastically in the past 4 years, due to growing infrastructure and modernization expenses.

Railways around the world, like in the US, Europe and Japan have undergone ownership changes. But, Indian railways continue to be monitored by the government.

In coming years, the Indian railways is all set to witness significant changes. The Indian Railways is planning to purchase locomotives, coaches, train sets, Electric Multiple Units (EMUs) from private manufacturers instead of buying them from the state-run companies

MARKET DYNAMICS

The Indian railways’ plan of exporting its coaches in the global $55 Billion rolling stock market will be a major growth driver for the rolling stock market in India. New coach manufacturing in India has already got a boost by record high CAPEX allocation of ~$900M in the FY 2019-20 budget, a sharp increase as compared to just ~$500M in FY 2018-2019.

METRO RAIL ROLLING STOCK MARKET IN INDIA

| Parameter | Operational | Under construction | Approved |

| Metro networks | 10 | 7 | 9 |

| Coaches | 1,500+ | 800+ | 1000+ |

| Type of cities | Tier-1- 7, Tier- 2- 3 | All tier-2 | All tier-2 |

As of Oct 2020, there are 10 metro networks in India with more than 1,500 coaches. By 2025, the number will go up to 25+ networks with 3,500+ coaches, creating demand for 2000+ additional coaches.

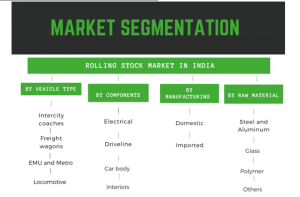

MARKET SEGMENTION

MARKET SIZE AND FORECAST

The Indian railway industry was a completely closed industry in the sense that most of the manufacturing and operations of rolling stock was carried out by the state-owned companies. But now, in FY 2019-2020, all of that is set to change. The railways will have 150 private trains by 2023 to start with and the routes that will go for bidding are still being worked upon. During bidding, the operators will be given options — import, buy rakes from an Indian company or on lease.

This move has made the Indian rolling stock market very attractive for International rolling stock suppliers and component manufacturers alike.

The dedicated freight corridor between Delhi-Mumbai, Delhi-Kolkata will also create new demand for cargo wagons as the new corridor will support max speed up to 100kph against existing 60kph.

The corporatisation of rail manufacturing is essential for upgrading the intercity trains to a max speed capability of 160-200kph from 110-130kph presently.

The rolling stock market in India will be worth ~$5 Billion or ~37,000 Crore INR by 2025

WHO MANUFACTURES ROLLING STOCK IN INDIA

As of Oct 2020, there are three state owned coach manufacturing facilities in India with a combined manufacturing capacity of ~4,200 coaches per annum. Hyundai Rotem, Bombardier are among the popular choice of metro network operators in India but they do not manufacture locally.

Alstom India and BEML– a state owned enterprise manufactures metro coaches, and EMUs apart from the three state owned companies.

RECENT DEVELOPMENTS IN ROLLING STOCK MARKET IN INDIA

July 2020- Indian Railways invited global tender from private companies to run trains on 109 routes. The private trains are proposed to be run in 12 clusters across the railway network

June 2020- More than 2,45,400 bio-toilets were fitted in 68,800 rail coaches, taking installation of bio toilets to 100%.

Feb 2020: India’s Bangalore Metro Rail Corporation Ltd. (BMRCL) awarded a Rs. 1,578 Crore ( @ 7.3 crore per coach, cheapest metro bid cost ever)contract to China’s CRRC Corporation’s subsidiary for 36 train sets consisting of 216 coaches

Oct 2019– BEML which has ~almost 50% market share in metro cars in India inaugurated a bogie and traction motor testing facility at its metro car manufacturing plant at the BEML Bangalore Complex

Oct 2019–Indian Railways planned to invite private domestic and international operators to bid for operating passenger trains on a lease basis on 25 inter-city routes covering distances from 500-700km.Private operators will be required to pay haulage fees along with the lease fee

Oct 2019- Indian Railways planned to procure 100 new trains by 2022 to increase the speed of services. Initially seven trains will be imported and the remaining trains will be manufactured in India under a technology transfer arrangement

Oct 2019–Indian Railways planned to convert all LHB trains to HoG(Head on generation) system by the end of this year. HOG taps power supply overhead power lines and distributes it to train coaches and does not need a power generator car(reducing 105 DB per car)

July 2019- The Finance Minister of India announced that the state does not have funds to make heavy investments($700 Billion) required to modernize Indian Railways between 2019-2030. Hence, the PPP(Public private participation) model is being considered

May 2019– There was a backlog of 25,000 freight wagons, due from private suppliers. The state owned indian railways has a wagon manufacturing capacity of just 4,000 units per annum. Coal and coke account for ~60% of freight traffic, followed by cement and foodgrains in India

COMPETITIVE LANDSCAPE

In the metro rolling stock market in India, State owned company, BEML holds the majority of fleet size in the country with ~40% share. BEML’s fleet is spread across Bangalore, Delhi, Kolkata and Jaipur metro lines. It is also estimated to deliver its first set of train sets to Mumbai in December 2020.

BEML’s strong reach in India, Alstom + Bombardier’s aggressive growth in the metro segment, and new entrant CRRC’s explosive penetration strategy will be key strategies to look out for, especially in the urban metro segment.

ICF Chennai, has stopped building conventional passenger coaches in the last two years.Vande Bharat Train is the High Speed EMU manufactured in India and is estimated to be produced at least 40% cheaper than the similar train in European countries.

THIS REPORT WILL ANSWER FOLLOWING QUESTIONS

- Market size and forecast of Rolling stock market in India, by application and vehicle type

- Opportunity for traction motor, HVAC, signaling, pantograph, seats and auxiliary suppliers in the rolling stock market in India

- Details on new rolling stock development and infrastructure upgradation of Indian railways

- Market share of major vendors

- Key criterion for vendor selection by Indian railway

- Growth strategy of leading rolling stock suppliers

- Average B2B prices, by rolling stock type

- Recently awarded rolling stock contracts by vehicle type